When activity-based costing (ABC) was introduced over 25 years ago, it quickly became a “board room” topic. Little wonder, as it was successfully used to drive countless [overhead] cost reduction and profitability improvement programs. I personally experienced how it provided insights that lead to hundreds of millions in value creation.

Globalization has made ABC even more relevant today. Why? Because manufacturers find it even more difficult to cope with functional silos – one of the primary causes of complexity-driven overhead costs. In fact, functional silos continue to erode value, while remaining a key barrier to achieving most strategies being pursued by global manufacturers.

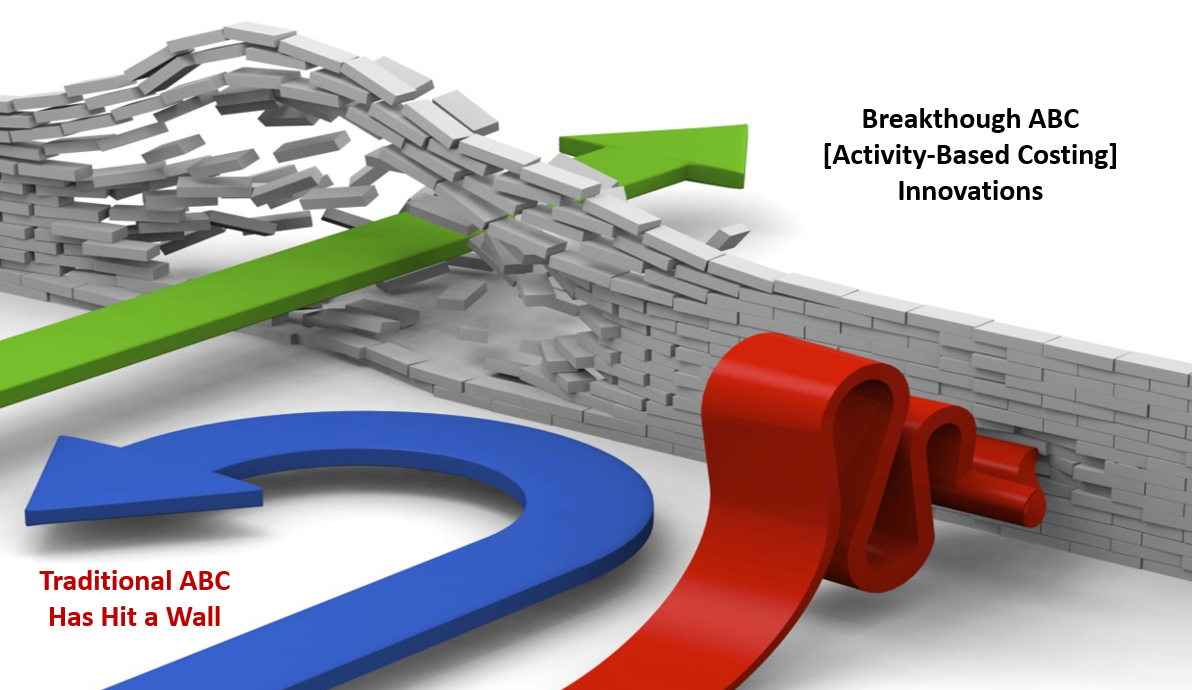

In light of this, one would think that [the use of] ABC would be even more prevalent today. But this isn’t the case. ABC has lost its luster. Its perceived effectiveness as a management tool has fallen. It now lags well behind analytics and other management approaches and technologies as the “tool du jour”. Three interrelated factors prevent ABC from being more effectively employed [as an ongoing management tool] in global manufacturers:

-

-

-

- ABC costing models often require significant time and effort to maintain, making them less attractive as ongoing management tools.

- ABC is not always part of ongoing performance management because it has not been effectively embedded into planning, budgeting & rolling forecast processes.

- ABC software typically lacks operationally-realistic planning models that can cope with manufacturing complexity. As a result, they aren’t typically viewed as tools that can support strategic, financial and operational decision making.

-

-

ABC software companies never fully addressed these issues. Which is one reason why so few of them remain. What’s more, they’ve provided little innovation in embedding process and systemic thinking into how global manufacturers plan, manage and govern their business. Additionally, improvements [that have been made] have been done in a vacuum. For example, while ABC pundits were busy talking about “time-based ABC”, they didn’t see that prescriptive analytics and supply chain optimization software had taken activity planning well beyond its traditional roots.

Mature forms of Activity-Based Costing / Planning incorporate Prescriptive Analytics,

While Integrating Strategic, Financial & Operational Management Processes

The good news is that technology innovations now address these issues. But not from traditional ABC and financial planning sources. I wrote about these innovations in a series of articles for FP&A Trends – a publication for Financial Planning & Analysis [FP&A] professionals.

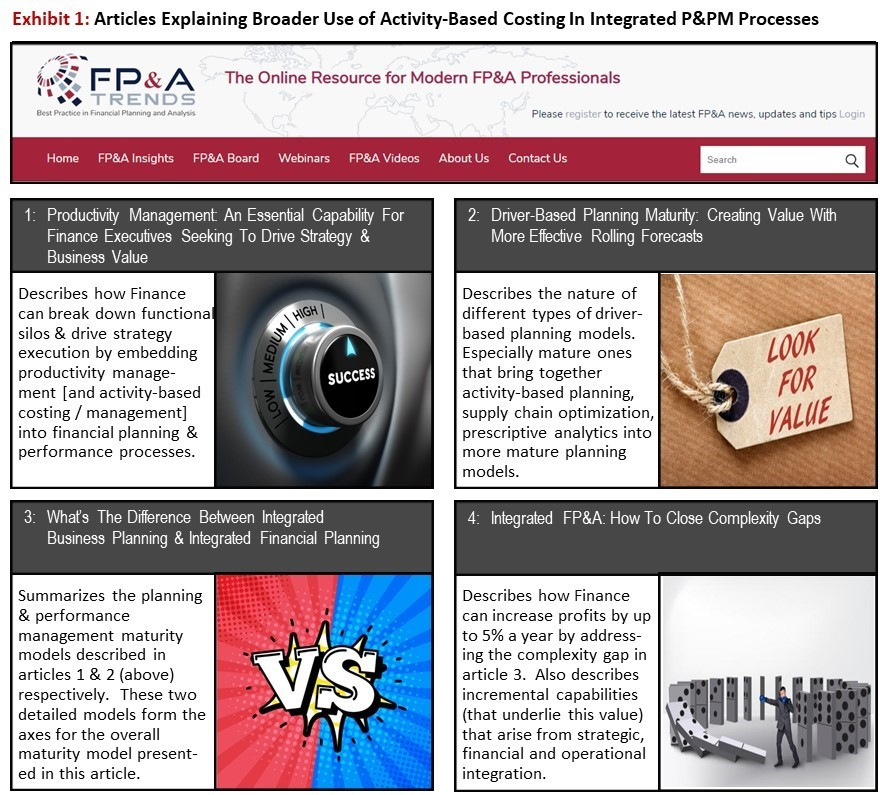

The innovation addressed by the articles is integrated [strategic, financial and operational] planning and performance management [P&PM] processes. The articles are summarized below, with the numbers corresponding to the article numbers in exhibit 1. They describe:

-

-

-

-

- Embedding activity costs into rolling forecast processes that support “Productivity Management” – a capability for breaking down functional silos.

- Integrating activity-based planning, supply chain optimization and prescriptive analytics into a single model / application to support outcome-based P&PM processes.

- How the capabilities [described in the first two articles] support mature processes that integrate all aspects of strategic, financial and operational P&PM.

- Four incremental capabilities created by integrated P&PM processes and why they can be worth 5% of sales to global manufacturers.

-

-

-

The link to Article 3 is provided here, with links to the other three shown at the bottom of it: https://www.fpa-trends.com/article/whats-difference-between-integrated-business-planning-and-integrated-financial-planning.

I believe that ABC has a significant role to play in driving strategy execution in global manufacturers. Particularly strategies that are founded upon superior cross functional execution, like operational excellence, profitable growth and sustainable cost reduction. Not in its present form, but in more mature ones that embed ABC into integrated P&PM processes that provide the means to effectively manage complexity-driven costs.